Technical debt in private equity deals used to be a footnote. Picture the diligence process on a software business five years ago: the technical team would review the platform, flag legacy components, note the debt, and factor it into a risk section of the memo. Then the deal team would weigh the revenue, the customer base, the market position, and decide whether the price still made sense. Technical issues were, in most cases, a negotiating point at the margins, not a primary driver of how the business was valued.

That calculus has changed. And for sellers who haven’t caught up to it, the change is expensive.

How Buyers Now Price Technical Debt in Private Equity Deals

There was a time when technology was treated as an operational detail in many deals.

If the business was performing, customers were stable, and revenue was growing, underlying platform issues could be deferred. Technical debt, fragmented systems, or legacy architecture were often accepted as part of the package, something the next owner could address.

That is no longer the case.

Today’s buyers approach technology with a fundamentally different lens. They are not just evaluating what a system does. They are evaluating what it will take to evolve it.

Scott Darby, a board member at Gorilla Logic who advises private equity firms on technology strategy across the hold period, describes the buyer posture this way: when technical debt is present, buyers assume the worst. They don’t underwrite the best-case remediation scenario. They underwrite the risk, build in a buffer for what they don’t know, and reduce the price accordingly.

The result is that technical risk has become a pricing mechanism. It shows up either as a direct discount to the purchase price, or as extended diligence timelines that give buyers more opportunity to find additional problems, neither of which serves the seller.

The Economics of Technical Debt in Private Equity Valuations

Valuation in private equity is fundamentally about confidence. A buyer is paying today for a stream of future cash flows they believe they can grow. Anything that introduces genuine uncertainty into that picture (about growth rates, integration complexity, or the durability of the business model) reduces what a rational buyer will pay.

Technical debt introduces uncertainty into all three. Poorly documented systems make it hard to predict how a platform will behave under the stress of integration or rapid scaling. Tightly coupled architecture slows product development and makes customer experience harder to maintain. Legacy infrastructure that requires significant specialist knowledge to operate creates key-person risk that buyers have to account for.

None of these problems are fatal on their own. But collectively they make the future performance of the business harder to model, and harder to model means lower confidence, and lower confidence means lower price. In competitive processes, where the difference between the winning bid and the second bid can be measured in fractions of a turn on EBITDA, that discount can be the difference between a successful exit and a disappointing one.

What’s Changed: Speed and the Accessibility of Modernization

Two forces are driving the heightened sensitivity to technical health, and both are accelerating.

The first is the pace at which modern software companies are expected to operate. Product cycles have compressed dramatically. Customer expectations for continuous improvement are higher than they’ve ever been. And well-funded competitors (often with leaner architectures and more modern engineering practices) can enter a market and iterate faster than incumbents can respond. A platform built for a slower era becomes a structural constraint on the growth that buyers are underwriting, compounding with every product cycle that slips.

The second force is subtler but important: modernization has become meaningfully faster and less expensive than it used to be. What once required a multi-year, eight-figure remediation program can now be executed in a fraction of that time with the right approach, tooling, and expertise. This changes the expectation. If a capable team can substantially address a company’s technical debt within the first phase of a hold period, buyers have little patience for carrying that debt into an exit. They know it could have been fixed. They price it as if it wasn’t.

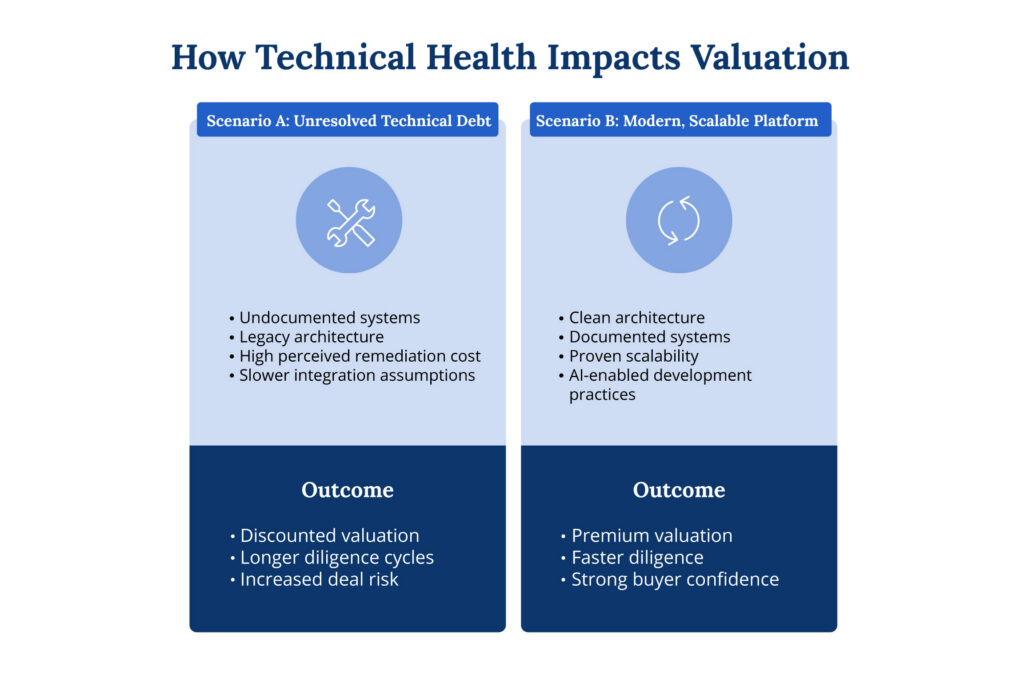

How Technical Health Impacts Valuation

Technical health directly influences buyer confidence, which in turn shapes valuation, deal velocity, and exit outcomes.

From Cleanup to Value Creation

One of the most important mindset shifts happening inside private equity is how modernization is framed. For a long time, resolving technical debt in private equity portfolios was treated as cleanup: something necessary, but not directly tied to value creation. A cost to absorb, not an investment to make.

That perspective is changing.

Modernization is now seen as a direct enabler of growth. And the firms that reframe technical debt in private equity as a strategic lever (rather than a background liability) are the ones arriving at exit with a fundamentally stronger story to tell.

A well-architected platform allows companies to:

- Integrate acquisitions more efficiently

- Launch new products faster

- Scale without significant rework

- Improve customer experience

These are not operational improvements. They are value drivers.

And when buyers evaluate a business, they are increasingly looking for evidence that these capabilities are already in place.

What Diligence Looks Like Today

Technical diligence has evolved from risk enumeration to capability assessment. The checklist has gotten longer and the questions have gotten harder.

Buyers are asking whether the architecture is genuinely scalable or whether current performance is masking underlying structural problems that will surface at the next inflection point. They’re asking how quickly new features can be developed and shipped, not in theory, but measured against actual release history. They want to understand the visibility of technical debt: is it tracked, understood, and actively managed, or is it a diffuse cultural tax that no one has ever fully quantified? And they’re assessing leadership: does the technology organization have the talent and discipline to sustain innovation through a transition?

These questions matter because buyers aren’t just evaluating what a business is today. They’re evaluating what it will take to get it to where they need it to be. A company with clean architecture, documented systems, proven scalability, and AI-enabled development practices tells a fundamentally different story than one without, even if both are generating comparable revenue today. The first is acquiring at a premium. The second is negotiating from a deficit.

The Real Cost of Deferring Technical Debt in Private Equity

There’s a persistent temptation inside portfolio companies to defer modernization until the business is performing well enough to afford the disruption. The logic feels reasonable: focus on growth first, clean up the tech when there’s more runway.

The problem is that this logic inverts the actual economics. Deferring modernization doesn’t eliminate the cost, it transfers it. Either the cost lands on the next buyer, who will price it into the transaction, or it lands back on the current owner through a lower exit valuation. Either way, someone pays. The question is who and when.

In a market where buyers are sophisticated enough to conduct serious technical diligence and experienced enough to know what they’re looking at, the sellers who carry unresolved technical debt to the table are effectively subsidizing their buyers. That subsidy comes directly out of exit proceeds.

The window to act is also shorter than most sellers appreciate. The majority of value creation in private equity happens in the first 12 to 24 months of a hold period, decisions made early compound through the hold, and decisions deferred early rarely get made at all. Technical strategy isn’t exempt from that dynamic. Companies that treat modernization as a pre-exit cleanup exercise typically discover they’ve run out of time to do it properly, and end up doing a rushed version that sophisticated buyers can identify immediately.

How Resolving Technical Debt in Private Equity Becomes Your Edge at Exit

Understanding that technical health matters for valuation is table stakes at this point. Most PE-backed technology businesses know this. The harder problem is executing modernization efficiently without disrupting the ongoing business, and doing it within the compressed timeframe of a hold period.

The most effective approaches aren’t wholesale transformation programs. They’re targeted, with clear prioritization of the highest-impact areas and an explicit connection between modernization work and business outcomes. They use AI and automation to accelerate delivery rather than treating modernization as a purely manual effort. And they bring in teams who have executed similar transformations before: not to outsource the work, but to transfer the knowledge and patterns that allow internal teams to sustain what was built.

The companies that get this right don’t show up to their exit with a technology platform that needs explaining. They show up with one that tells its own story: clean architecture, strong scalability evidence, documented systems, and a development organization that can demonstrate genuine velocity. That story commands a premium. It compresses diligence timelines. And it gives buyers the confidence to move quickly and pay accordingly.

Technical debt in private equity is no longer a background issue to be managed quietly. It’s a front-line factor in how businesses are valued, acquired, and positioned for growth. The firms that treat technical health as a strategic lever, and invest in it early enough to show up at the exit table with something to show for it, are the ones whose portfolio companies are consistently commanding better outcomes.

This post draws on a fireside chat between Scott Darby, Gorilla Logic board member, and Drew Naukam, Gorilla Logic’s CEO. They cover how buyers approach technical diligence today, what sellers consistently underestimate, and how to close the gap before it closes your multiple. Watch the full conversation here.